December turned out to be a good month for construction companies and producers of building materials, according to our latest monthly report “Construction market in Poland – February 2021”. However, the outlook for the construction industry in 2021 remains moderately bleak, mostly because of a high comparison base of Q1 2020. That the second half of the year could see an upturn is yet suggested by higher order books reported by the top 20 construction companies.

In H1 2021 the decline that the construction sector will face should not be significant because it is characterised by a low risk of COVID-19 spreading and a negligible administrative risk of construction being closed down entirely. Despite a slightly lower volume of investment projects, construction companies will be in a relatively more comfortable situation compared to such sectors as tourism, entertainment, or restaurants.

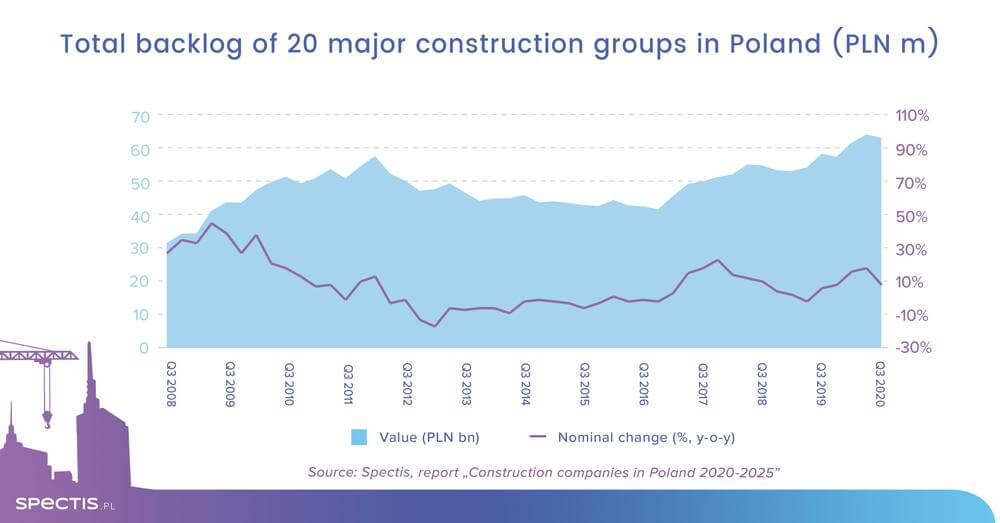

Small and medium-sized construction companies, which often stand in the role of subcontractors, have more reasons to worry over the first half of the year. The largest enterprises can look into the future with more confidence. In Q3 2020, the aggregate order books of the leading contractor groups grew at a rate of 8% year on year and their value stood at PLN 63bn (€15bn). The growth of the sector’s aggregate order book was fuelled by large-scale road construction contracts and industrial and power deals. However, some signs of a slowdown are apparent in order books of companies with substantial involvement in building construction projects. Companies involved in all types of construction activity have been observed to steadily shift towards the civil engineering construction segment.

An analysis of active contracts being handled by the top 25 contractors shows that Budimex, Porr, Strabag, Mirbud, Polimex-Mostostal, Mostostal Warszawa, Intercor, Gulermak and Astaldi are the groups currently engaged in the highest-value projects, mostly due to participation in large-scale road, railway, tunnel, and power contracts.

Among companies specialised in building construction, Skanska, Warbud, Budimex, and Porr report the highest value of contracts currently underway. Budimex, Erbud and Unibep are at the helm of the residential construction sector. Each of these groups is engaged in residential projects worth around PLN 700m-900m. Regarding the non-residential construction sector, Skanska and Warbud are the leading contractors, ahead of Budimex and Porr.

A weakness of the construction sector that will be evident throughout 2021 will be its natural delay in relation to the ongoing economic situation. Therefore, the construction industry is likely to see improved growth only in the second half of 2021. However, the scale of the recovery largely depends on an efficient implementation of the investment package co-financed under new EU funds.

Ask for free sample of report

info@spectis.pl